While the internal WebRTC world has seen a lot of famous company names attending conferences, participating in standards bodies, issuing press releases, or selling tools, SDKs or enablers to each other, relatively few have actually put out "powered by WebRTC" products into the real world for users.

Obviously, Google and Mozilla have both launched browsers, but that doesn't really count as that's still an "enabler" rather than an end-user product or service. There's also a ton of plucky startups like Bistri, Solaborate, Uberconference, Twelephone and others that have entered niches like conferencing and social networks, but none have yet hit maturity or been seen as major disruptions to the status quo in their sectors.

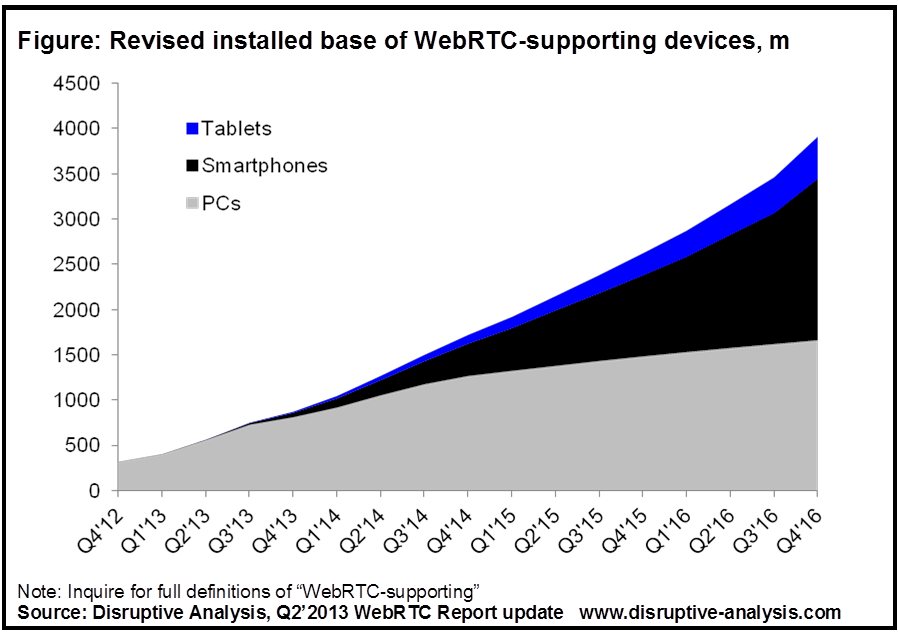

Buy the Disruptive Analysis WebRTC strategy report & market forecasts - now including the Q2 June 2013 update

To my mind, there are now three "traditional" big players that have walked the walk, and put WebRTC into their mainstream products:

First, the "big guns" are now coming out of hiding (or at least, out of their labs). One is an outlier, two is a coincidence, but three is a trend. I'd expect many of the others in each of these categories' peer groups to start using WebRTC over the next 6-9 months.

Second, there are no telcos in this list. The closest we've seen to market-ready WebRTC offers from SPs are AT&T's API work, and Telefonica's OpenTok and Mantis tools/platforms for developers. However, we haven't yet seen an end-user telco WebRTC proposition, although Telefonica is "eating its own dogfood" with its use of the TokBox-powered Oscar videoconferencing application internally.

Third, a lot of real-world WebRTC use is going to be hidden. There may well be a bunch of companies - banks, healthcare providers and so forth - using WebRTC "under the hood" in their websites, perhaps using call-me buttons, or gateways from Thrupoint or Oracle or Genband or others, without trumpeting it to the wider market.

Fourth, although enterprise deployments are still in the vanguard for WebRTC, the emergence of Vonage's solution raises the possibility that consumer mobile apps will rapidly deliver millions of active users. It's not just Chrome and Firefox browsers that update easily or automatically - most mobile apps do as well. It only takes one major social network to adopt WebRTC - not even for "calling" but maybe something data-related or other video use-cases - and I'm going to be reworking my forecast model again. To my mind, Vonage has been the big light-switch for a lot of people - mobile WebRTC isn't necessarily going to be browser based, but embedded into apps.

Fifth, startups are going to have to either act fast or differentiate solidly. Incumbents in most WebRTC-centric applications aren't going to be taking years to procrastinate and respond to disruptors. This puts a premium on marketing, distribution and sales, especially where newcomers are pitching directly against established players - videoconferencing, I'm looking at you! (I'll reserve judgement on some of the telecom use-cases' ability to accelerate though: let's see what happens).

Overall, it's good to see well-known players like Zendesk, Vonage & Siemens adopting WebRTC. It gives gravitas to the market and gives something for a couple of naysayers to chew on.

Let's see who's next: my money would be on the other UC vendors looking to spike Siemens' guns with brought-forward announcements, although we could conceivably see a VoIP/IM brand like Viber or Whatsapp surprise us as well.

If you're reading this and want more details about Disruptive Analysis' predictions for WebRTC, you should definitely buy the report - now available including the Q2 June 2013 update.

Obviously, Google and Mozilla have both launched browsers, but that doesn't really count as that's still an "enabler" rather than an end-user product or service. There's also a ton of plucky startups like Bistri, Solaborate, Uberconference, Twelephone and others that have entered niches like conferencing and social networks, but none have yet hit maturity or been seen as major disruptions to the status quo in their sectors.

Buy the Disruptive Analysis WebRTC strategy report & market forecasts - now including the Q2 June 2013 update

To my mind, there are now three "traditional" big players that have walked the walk, and put WebRTC into their mainstream products:

- Zendesk is a major player in SaaS-based customer support, enabling helplines or mail/IM interaction for big web companies and others. It has 30,000 customer companies and has facilitated support for over 200 million "customers' customers". It started to defaulting to WebRTC for voice calls a couple of months ago, on relevant browsers, while others still use Flash or other options. (It's worth noting that other startups such as Zingaya also have WebRTC-based B2C click-to-call buttons deployed for some large companies for support & CRM)

- Vonage created quite a stir at the WebRTC Expo in Atlanta last month. As one of the best-known VoIP players spanning home phonelines to mobile apps, it is the first of the big consumer communications brands to adopt the technology openly. It is also the first massmarket company to commercialise a non-browser, app-integrated variant of WebRTC, optimised for working on mobile devices. (Good interview with the CTO here). It's also pitching to provide white-label/partnered plaftorms for telcos. Outside the main scope of this blog post, but Vonage is apparently using the WebRTC Native Stack - the code mostly intended for browser suppliers - to build WebRTC into a non-browser app instead. It also claims several million users already, on both iOS and Android.

- Siemens Enterprise Communications is the first major enterprise UC player to throw its hat into the WebRTC ring with a (beta, pre-commercial) offering, called Project Ansible . At first sight, Ansible looks remarkably well-thought through, with social integration, fixed and mobile implementations, Hypervoice-type features ("Thought Trails") and, importantly, as much emphasis placed on design (courtesy of specialists frog) as engineering. The website discusses things like "joy of use" and "freemium models" - unusual for business comms tools from major vendors. Siemens has stolen a march on its big UC peers (albeit it with a beta) - despite Cisco being involved in WebRTC since Day 1, and an Avaya employee quite literally "writing the book". As yet, they haven't announced actual WebRTC products, though. Others like Microsoft are pursuing other strategies for now (Skype/Lync integration etc).

First, the "big guns" are now coming out of hiding (or at least, out of their labs). One is an outlier, two is a coincidence, but three is a trend. I'd expect many of the others in each of these categories' peer groups to start using WebRTC over the next 6-9 months.

Second, there are no telcos in this list. The closest we've seen to market-ready WebRTC offers from SPs are AT&T's API work, and Telefonica's OpenTok and Mantis tools/platforms for developers. However, we haven't yet seen an end-user telco WebRTC proposition, although Telefonica is "eating its own dogfood" with its use of the TokBox-powered Oscar videoconferencing application internally.

Third, a lot of real-world WebRTC use is going to be hidden. There may well be a bunch of companies - banks, healthcare providers and so forth - using WebRTC "under the hood" in their websites, perhaps using call-me buttons, or gateways from Thrupoint or Oracle or Genband or others, without trumpeting it to the wider market.

Fourth, although enterprise deployments are still in the vanguard for WebRTC, the emergence of Vonage's solution raises the possibility that consumer mobile apps will rapidly deliver millions of active users. It's not just Chrome and Firefox browsers that update easily or automatically - most mobile apps do as well. It only takes one major social network to adopt WebRTC - not even for "calling" but maybe something data-related or other video use-cases - and I'm going to be reworking my forecast model again. To my mind, Vonage has been the big light-switch for a lot of people - mobile WebRTC isn't necessarily going to be browser based, but embedded into apps.

Fifth, startups are going to have to either act fast or differentiate solidly. Incumbents in most WebRTC-centric applications aren't going to be taking years to procrastinate and respond to disruptors. This puts a premium on marketing, distribution and sales, especially where newcomers are pitching directly against established players - videoconferencing, I'm looking at you! (I'll reserve judgement on some of the telecom use-cases' ability to accelerate though: let's see what happens).

Overall, it's good to see well-known players like Zendesk, Vonage & Siemens adopting WebRTC. It gives gravitas to the market and gives something for a couple of naysayers to chew on.

Let's see who's next: my money would be on the other UC vendors looking to spike Siemens' guns with brought-forward announcements, although we could conceivably see a VoIP/IM brand like Viber or Whatsapp surprise us as well.

If you're reading this and want more details about Disruptive Analysis' predictions for WebRTC, you should definitely buy the report - now available including the Q2 June 2013 update.