Big news today - Microsoft has officially confirmed that it will be implementing ORTC (Object Realtime Communications) in future versions of IE, and that it will be integrating it with Skype. It's not planning to support WebRTC 1.0 it appears, but that has been pretty clear for a long time. (At least, it's what I've assumed in my own forecasts anyway). ORTC has been labelled as WebRTC 1.1, although it's still not an "official" standard but a "community" enhancement.

Details are still only in outline. The most controversial aspect will be the support of H.264 video codec rather than VP8, although that's hardly surprising given that (a) there has been no agreement on mandatory codecs yet anyway, and (b) VP8 is obviously a very Google-centric technology. Given that Firefox is supporting both, and Apple is definitely an H.264 fan, some will find this annoying but hardly surprising.

My take has long been that a certain level of fragmentation is OK for most WebRTC use-cases and developers. It's a bit of a pain, but it's not the end of the world. Yes, there will be questionmarks about licensing / royalty fees, but if that's picked up by the browser supplier (or third parties like Cisco) that should be tractable.

I'd expect most of the WebRTC cloud platform providers to support ORTC endpoints - which may mean that the cloud/gateway model of WebRTC gains even more traction vs. pure peer-to-peer use cases. (The cloud approach was growing anyway, as it's the main way to support WebRTC-type voice/video inside iOS and Android apps).

Frankly, the details are important but manageable. We can safely ignore the usual anti-Microsoft brigade's whining about this; Google has worked on the ORTC spec alongside Microsoft and Hookflash, and it is widely (albeit not universally) seen as a good approach, especially as WebRTC 1.0 uses an arcane approach called SDP (a legacy of SIP) to set up connections.

There are still unanswered questions, which should hopefully get clarified in due course:

The bottom line is that this is a good day for the "democratisation of voice and video communications" - one way or another, most browsers from mid-2015 onward will be able to support embedded communications directly into websites. Given the various cloud platforms and plug-ins available to smooth the path for developers, this is yet another sign that WebRTC (including ORTC) is proceeding along the right path.

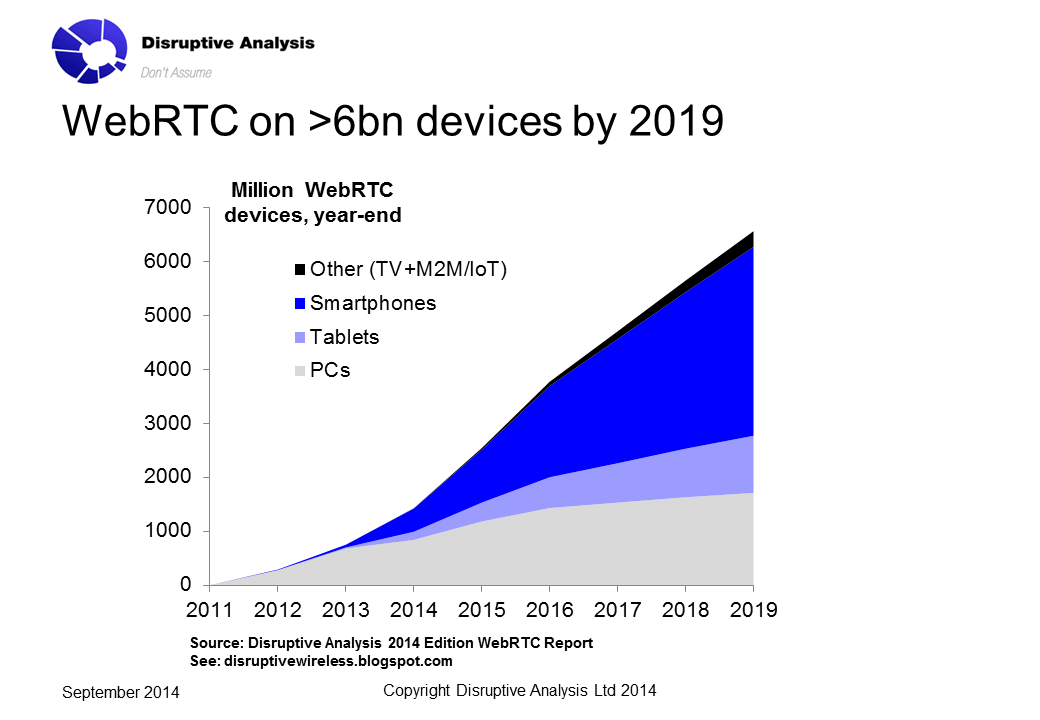

I'm maintaining my view that there will be upwards of 2 billion active individual users of WebRTC by 2019 - a large proportion of the overall Internet and smartphone app user-base. For more details about use-cases, strategic analysis of Microsoft's & Apple's roles, see my full report published recently. Purchasing details are here.

Details are still only in outline. The most controversial aspect will be the support of H.264 video codec rather than VP8, although that's hardly surprising given that (a) there has been no agreement on mandatory codecs yet anyway, and (b) VP8 is obviously a very Google-centric technology. Given that Firefox is supporting both, and Apple is definitely an H.264 fan, some will find this annoying but hardly surprising.

My take has long been that a certain level of fragmentation is OK for most WebRTC use-cases and developers. It's a bit of a pain, but it's not the end of the world. Yes, there will be questionmarks about licensing / royalty fees, but if that's picked up by the browser supplier (or third parties like Cisco) that should be tractable.

I'd expect most of the WebRTC cloud platform providers to support ORTC endpoints - which may mean that the cloud/gateway model of WebRTC gains even more traction vs. pure peer-to-peer use cases. (The cloud approach was growing anyway, as it's the main way to support WebRTC-type voice/video inside iOS and Android apps).

Frankly, the details are important but manageable. We can safely ignore the usual anti-Microsoft brigade's whining about this; Google has worked on the ORTC spec alongside Microsoft and Hookflash, and it is widely (albeit not universally) seen as a good approach, especially as WebRTC 1.0 uses an arcane approach called SDP (a legacy of SIP) to set up connections.

There are still unanswered questions, which should hopefully get clarified in due course:

- Will ORTC pop up in IE12 or IE13 first? Will it initially be launched in beta, and under what conditions?

- Will ORTC support DataChannel properly?

- What happens with Lync? How does that fit into the ORTC/IE landscape?

- Might Microsoft support VP8 in a future release, anyway? Or does that depend on how the market evolves?

- When will ORTC make its way into Windows Phone, and how?

- Will Microsoft use its Azure cloud platform to offer WebRTC as some form of managed service to developers?

- What toolkits and support will Microsoft offer to developers for ORTC?

- Will we see WebRTC/ORTC support in Dynamics CRM, X-Box or other Microsoft properties?

- Does this limit the scope for 3rd-party IE WebRTC plug-ins (eg Temasys') or does it legitimise them, as a way of getting RTC capability into IE11 and below?

The bottom line is that this is a good day for the "democratisation of voice and video communications" - one way or another, most browsers from mid-2015 onward will be able to support embedded communications directly into websites. Given the various cloud platforms and plug-ins available to smooth the path for developers, this is yet another sign that WebRTC (including ORTC) is proceeding along the right path.

I'm maintaining my view that there will be upwards of 2 billion active individual users of WebRTC by 2019 - a large proportion of the overall Internet and smartphone app user-base. For more details about use-cases, strategic analysis of Microsoft's & Apple's roles, see my full report published recently. Purchasing details are here.