I've just spent two days at an event called Nexterday North, run by Finnish OSS specialist CompTel. It wasn't the usual vendor product-based user conference, but more a quasi-TED flavoured "anti-seminar" with assorted general futurists (notably Rohit Talwar and Patrick Dixon), as well as outspoken telco-industry provocateurs like myself and Alan Quayle. It was fun and refreshing, held in a warehouse by the Helsinki docks. My talk was on "Top 10 Myths in Telecoms" and will be uploaded to the event site soon.

There were also some good, high-level operator presentations. Tele2 and Globe (from the Philippines) has some interesting angles, but the one that really struck me was SoftBank's.

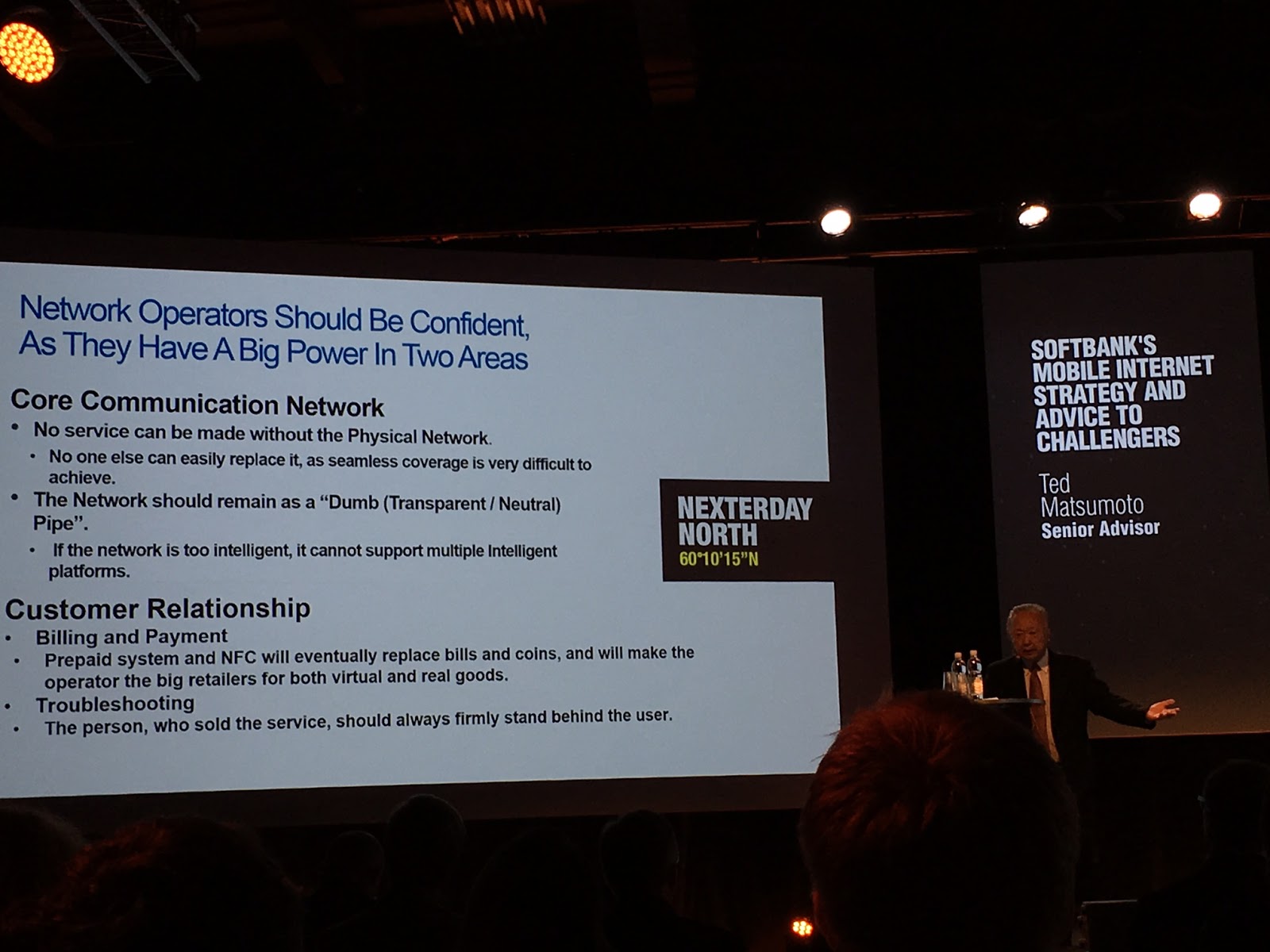

A bit of history - SoftBank is basically a web and software company with a fixed broadband arm, that bought a mobile operator (Vodafone Japan) rather than vice versa. It also now owns Sprint in the US. The Japanese mobile profits are now 9x what they were under the VF stewardship of the business, and it has increased its market share considerably.

But at the same time, the company has been involved in numerous other successful Internet businesses, notably Yahoo Japan and a major stake in Alibaba. More recently it has invested in Indian online players SnapDeal and Ola.

The key point that the speaker made was that the network businesses and service businesses are decoupled. Yes, there are certain services that are integrated - the mobile network has telephony and so forth. But SoftBank's mobile network activities were specifically described as being the much-derided "dumb pipe" model, with heavy utilisation of both WiFi (both in homes and public hotspots) for offload / load-balancing.

I'd disagree with the assertion that mobile operators will benefit from NFC payments, but that may be different in Japan as an exception. (Although last time I was in Tokyo, nobody used NFC for train tickets - I stood watching people coming through the barriers in Shinjuku Station).

But the key message is that as a network operator the money comes from driving data traffic usage, whilst keeping costs manageable. There was no angst about so-called "OTTs". Virtualisation and heavy use of indoor coverage solutions are seen as critical, especially given the urban-heavy bias of Japan mobile usage. (Sidenote: global urbanisation was seen as a trend by numerous speakers; a topic for another post).

The reason for the lack of concern about OTTs is that SoftBank is "hedged". It has its own Internet/online footprint and benefits from the growth of the web (and, implicitly, neutrality).

So while the Japanese network business is looking to create some network-based services (it has implemented VoLTE for example) this is not the core of its overall Group-level hopes for deriving value from the web and apps. It is, in reality, there to support the sales of data network services.

The real value comes from entirely separate ecosystems like Alibaba - which primarily derives revenues from people and countries for whom SoftBank doesn't offer connectivity. In other words: "The upper layer and lower layer has no need to be integrated".

In many ways this is like the oil industry. Many major integrated companies do exploration and production (E&P) in areas of the world where they do not also do refining and marketing (R&M). They produce crude oil in one place (analogy: network capacity) and process/consume it in others (analogy: network traffic & applications). It's not a perfect metaphor because there's a global marketplace for crude, but it's a useful conceptual tool.

SoftBank is successful on both sides of the connectivity/application divide because it does not try to integrate them. Its recent investment in the Indian Internet industry is because it sees growth in its own right, not as a way to "add value" to its network assets. Meanwhile most other telcos try to "leverage the network" with IMS, QoS, complex policy-control, APIs, numbering, integrated IoT platforms and so on.

As far as I know, none of the SoftBank Internet businesses is particularly interested in "specialised services", paid priority or any of the other non-neutrality myths. Maybe there will isolated examples in future, but the bulk of its "digital" activities just use plain, vanilla, Internet access.

Verizon is perhaps heading in the right direction with its purchase of AOL (although one could question the choice of target). Telefonica's TokBox remains the rare example of a telco-owned Silicon Valley company that hasn't been messed up by its new owners, three years after acquisition. But for now, SoftBank is the pre-eminent example of a successful dual telco + Internet strategy. It exemplifies what I was referring to when I first talked about Telco-OTT businesses, 4 years ago.

Other operators should take its lessons to heart, and decouple network and Internet business units. Regulators should consider whether structural separation would be healthy for the industry, if they don't do it themselves.

There were also some good, high-level operator presentations. Tele2 and Globe (from the Philippines) has some interesting angles, but the one that really struck me was SoftBank's.

A bit of history - SoftBank is basically a web and software company with a fixed broadband arm, that bought a mobile operator (Vodafone Japan) rather than vice versa. It also now owns Sprint in the US. The Japanese mobile profits are now 9x what they were under the VF stewardship of the business, and it has increased its market share considerably.

But at the same time, the company has been involved in numerous other successful Internet businesses, notably Yahoo Japan and a major stake in Alibaba. More recently it has invested in Indian online players SnapDeal and Ola.

The key point that the speaker made was that the network businesses and service businesses are decoupled. Yes, there are certain services that are integrated - the mobile network has telephony and so forth. But SoftBank's mobile network activities were specifically described as being the much-derided "dumb pipe" model, with heavy utilisation of both WiFi (both in homes and public hotspots) for offload / load-balancing.

I'd disagree with the assertion that mobile operators will benefit from NFC payments, but that may be different in Japan as an exception. (Although last time I was in Tokyo, nobody used NFC for train tickets - I stood watching people coming through the barriers in Shinjuku Station).

But the key message is that as a network operator the money comes from driving data traffic usage, whilst keeping costs manageable. There was no angst about so-called "OTTs". Virtualisation and heavy use of indoor coverage solutions are seen as critical, especially given the urban-heavy bias of Japan mobile usage. (Sidenote: global urbanisation was seen as a trend by numerous speakers; a topic for another post).

The reason for the lack of concern about OTTs is that SoftBank is "hedged". It has its own Internet/online footprint and benefits from the growth of the web (and, implicitly, neutrality).

So while the Japanese network business is looking to create some network-based services (it has implemented VoLTE for example) this is not the core of its overall Group-level hopes for deriving value from the web and apps. It is, in reality, there to support the sales of data network services.

The real value comes from entirely separate ecosystems like Alibaba - which primarily derives revenues from people and countries for whom SoftBank doesn't offer connectivity. In other words: "The upper layer and lower layer has no need to be integrated".

In many ways this is like the oil industry. Many major integrated companies do exploration and production (E&P) in areas of the world where they do not also do refining and marketing (R&M). They produce crude oil in one place (analogy: network capacity) and process/consume it in others (analogy: network traffic & applications). It's not a perfect metaphor because there's a global marketplace for crude, but it's a useful conceptual tool.

SoftBank is successful on both sides of the connectivity/application divide because it does not try to integrate them. Its recent investment in the Indian Internet industry is because it sees growth in its own right, not as a way to "add value" to its network assets. Meanwhile most other telcos try to "leverage the network" with IMS, QoS, complex policy-control, APIs, numbering, integrated IoT platforms and so on.

As far as I know, none of the SoftBank Internet businesses is particularly interested in "specialised services", paid priority or any of the other non-neutrality myths. Maybe there will isolated examples in future, but the bulk of its "digital" activities just use plain, vanilla, Internet access.

Verizon is perhaps heading in the right direction with its purchase of AOL (although one could question the choice of target). Telefonica's TokBox remains the rare example of a telco-owned Silicon Valley company that hasn't been messed up by its new owners, three years after acquisition. But for now, SoftBank is the pre-eminent example of a successful dual telco + Internet strategy. It exemplifies what I was referring to when I first talked about Telco-OTT businesses, 4 years ago.

Other operators should take its lessons to heart, and decouple network and Internet business units. Regulators should consider whether structural separation would be healthy for the industry, if they don't do it themselves.

2 comments:

Nice post, Dean.

From a purely architectural standpoint, using the well-accepted Core-Distribution-Access structure, end-user services should be implemented in the core, not at the access layer. Once you concede that mobile is just one more form of access to the 'public core', it really doesn't make much sense to continue advocating for end-user service development that is inextricably linked to the mobile network. I'd argue that IMS/VoLTE is supportive of this argument, as it also provides voice/messaging services via alternate / non-cellular access.

A corollary to the above is that coupling end-user services with access technologies slows down their development, especially if done through standards setting bodies. Services are evolving in 'dog years', while access technologies tend to advance at a much more methodical pace. Linking the former to the latter is not a recipe for success in the 21st century.

Cheers,

Dave

Dave,

Don't be so certain that access technologies are moving at a glacial pace. Just look at what is occurring in the LAN and PAN wrt to 802.11 and BLE when it comes to IoT. It is the vertically integrated carrier access layers (MSOs, MNOs, Telcos) that are moving at glacial speed because their investment in capex and opex at every layer is not being sufficiently amortized. Just this past week Verizon indicated it is stepping up its wireless investment and moving aggressively to 5G. That hasn't fully sunk into analysts forecasts and without significant new subscribers and with video capacity wars looming (with T-Mo's announcement) it's likely that analysts will finally question the vertically integrated strategy.

But I agree with your conclusion that wireless is just another access medium and not a stand-alone architecture and business model in the long-run.

Dean,

Just to clarify, do you see the divide as an east-west or north-south issue?

Michael

Post a Comment