Private 4G and 5G networks are rapidly becoming mainstream. This isn’t news.

But

from recent conversations, client engagements and events, it’s becoming

increasingly clear that many don’t quite grasp how private cellular

use-cases are segmented – and why it’s going to get even more complex in

the next 2-3 years.

In reality, this isn’t really “a market” in a singular sense. It’s currently at least three separate and distinct markets, with only minimal overlap at present. The main common thread is the deployment of cellular (3GPP 4G/5G) networks by non-MNOs.

A

common fallacy involves talking about “vertical industries” as the main

way to divide up the sector. But that doesn’t really work, as any given

vertical has dozens of sub-categories and hundreds of potential

applications and deployment scenarios. For instance, the “energy

vertical” covers everything from a gas station, to an offshore windfarm,

a 1000km pipeline or an oil-futures trading floor in a financial

district.

Verticals are useful ways to divide up sales and

marketing efforts, and make sense for cohesive reports, papers or

webinars, but also blend together elements of three very different markets for private 4G/5G:

- Critical communications networks

- Indoor mobile phone networks

- Cloud and IT/IoT networks

It is worth discussing each of these in turn.

Critical communications networks

These

have made up the bulk of major private network deployments over the

last 5-10 years. They are typically deployed for utilities, oil &

gas, mining, public safety, airports and military purposes. Often, they

are used in rugged environments, for human communications (typically

push-to-talk), as well as in-vehicle gateways and specific automation

systems such as remote sensors and monitoring systems. The specialised

GSM-R system for railways fits in this category as well.

Usually,

they are replacing alternatives such as private mobile radio (PMR),

TETRA and microwave fixed-links. They have typically been packaged and

deployed by specialist integrators for sectors like oil-rigs or

field-deployment by military units. There is limited “replicability”.

They vary widely in size, from a single portable network for public

safety, up to a national network for a utility company.

There is

little need for interconnection with public mobile networks; indeed it

may be specifically avoided in order to maintain isolation for optimal

security and “air-gapping” for critical applications.

Most are 4G,

reflecting mission-criticality and its frequent need for proven, mature

technology and wide product availability. 5G is however used in certain

niches and is being tested widely, although the most useful features

will only arrive when Release 16/17 versions are commercialised in the

next few years.

Indoor mobile phone networks

This includes

some of both the oldest and newest deployments. Early local private

2G/3G networks essentially used GSM phones and thin slices of

light-licensed/unlicensed spectrum to replace DECT cordless phones in a

few markets – notably the UK, Netherlands and Japan.

They could

also work with multi-SIM phones to blend public and private modes. I

first saw an enterprise-grade GSM picocell in 2001, and an on-premise

core network box in 2005. There are still several thousand such networks

around, including ones updated to 4G and some that run on ships or

onboard private jets.

More recently, there has been growing

interest in using private 4G/5G to create neutral host networks for

in-building, or on-campus coverage. There are multiple models for

neutral host (I’ve counted around 10-15 variations), with some needing a

full local network with its own spectrum and core, and others just

relying on the tenant MNOs’ active equipment. In the US, CBRS-based

options may turn out to be among the more sophisticated.

Whether

used to support public MNOs more effectively than alternative indoor

systems such as DAS (distributed antenna systems), or perhaps for

linking to a UC / UCaaS system for enterprise voice, the main use-cases

are for phones. They are almost always deployed for a single building or

campus.

This segment is the most likely to require

interconnection with the public mobile infrastructure, as well as

supporting normal “phone calls” rather than push-to-talk voice.

Cloud and IT/IoT network

This

category of private cellular is probably receiving the greatest

attention from many newcomers to the sector, as well as external

observers such as analysts and journalists.

It ties in with many

of the newest trends around cloud and edge-computing, AI and machine

vision in factories, robots and AGVs in warehouses, security cameras and

more general IoT / smart building use-cases. It aligns with many of the

"transformation" projects in IT, plus some parts of the OT (operational

technology) space such as smart manufacturing.

As such, it tends

to be viewed as a complement – or alternative – to other IT-type network

technologies like Wi-Fi and fibre-based ethernet. And given that many

of the use-cases have a heavy cloud (or at least multi-site WAN)

orientation, there is more acceptance of virtualisation of cores and

perhaps in future the RAN.

This is currently the area with the

greatest amounts of experimentation and innovation – although actual

large-scale operational deployments are still relatively few. There is

more focus on 5G than 4G, although that might change as executives learn

more about the practicalities and economics. Vendors often orient on

the soundbite that "private 5G should be as easy as Wi-Fi".

There

is a major focus on automation, replicability and ease-of-use. This was

exemplified by the recent AWS Private 5G announcement, which seems

squarely aimed at this segment.

However, there is perhaps a divide

opening between the IT-type scenarios (where it can be seen as a sort

of enterprise Wi-Fi-on-steroids vision) and OT deployments in which it

gets embedded into larger industrial automation or other systems, such

as factory robots or dockside cranes. In the latter scenarios we can see

companies like Siemens integrating cellular into their wider systems,

just as they have historically used Wi-Fi/WLAN and fibre.

Although

the main focus is on building / campus networks for this model, it may

also extend to larger domains such as smart cities, as well as

multi-location users such as retail chains.

There is some

overlap with the critical communications segment, but that is fairly

rare at the moment, especially given the lesser role (and trust) of

public cloud in many of those areas.

In addition, there is a fair

amount of talk about interconnection with the public mobile network

(especially where telcos are acting as vendors), but in reality, that's a

secondary consideration that doesn't go much beyond a PowerPoint slide

for now. There are certain exceptions which are interesting, but they're

far from typical.

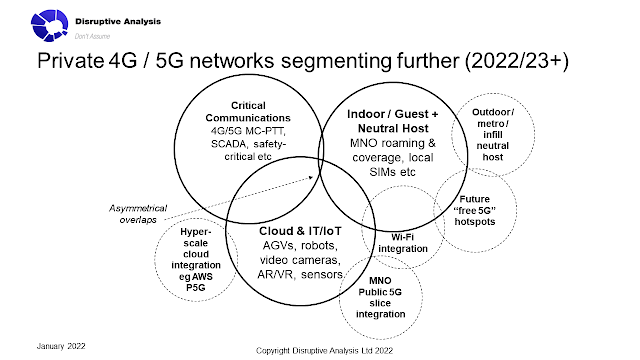

Conclusions and the Future of Private Networks Segmentation

At

present, the "private 5G market" is actually at least three separate

markets. And it's mostly about private 4G rather than 5G. Critical

communications networks, indoor mobile phone networks and cloud/IT/IoT

networks are largely distinct in terms of motivations, channels,

economics, devices and applications. There is much less overlap than

many observers expect.

(There are also smaller adjacent sectors such as community networks, 4G/5G-based FWA and other specialities).

But

over the next 1-2 years, we can expect the three bubbles on the Venn

diagram to overlap more – although asymmetrically. Critical and

cloud/IoT networks will start to become hybridised. Critical 4G/5G

networks in mines or utility sites will start to support extra IT-like

applications, for instance (although that probably won't need formal

network slicing).

Some enterprise private cellular networks will

examine adding neutral-host and inbound roaming or interconnect from

public MNOs' subscribers – although there are assorted regulatory and

security/operational hurdles to address.

There won't be much

overlap between critical networks and neutral/guest cellular, though.

Nobody's smartphone will be roaming from their normal consumer 5G

network onto the utility company's private infrastructure, I think. A

few employees' devices might have special arrangements though.

But

we will also see the emergence of a number of additional bubbles on the

chart, some of which are more like "quasi-private" models, such as

outdoor neutral host networks, selling wholesale capacity to MNOs. There

will be various forms of Wi-Fi integration (but probably less than many

expect / want). And we will undoubtedly see maturity of both

cloud-delivered private cellular like AWS's, and (belatedly) some sort

of MNO-based network slice integration.

And if you want an

"outlier" to ponder, consider the potential for grassroots private

"consumer-grade" 5G. There's a lot of hype about things like Helium's

decentralised and blockchain-based model, but I'm deeply sceptical of

this (that's for another post, though). More likely is the emergence of a

true Wi-Fi hotspot approach, where we start to see lightweight "free

5G" options, using unlicensed (or maybe CBRS GAA) spectrum, with a cheap

core and small cell. Scan the QR code next to the barista to download

your eSIM, and you're good to go….

The bottom line is that the

private 4G/5G market is complex and nuanced. Market statistics

frequently combine everything from a nationwide utility's or railway's

critical infrastructure, to a few small-cells connecting up digital

signs in a mall car-park. It's easy to assume it's all about

millisecond-latency robots zipping about factories, rather than a

security guard with a handheld radio, or indoor network coverage for a

hotel.

Operators, vendors, enterprises and governments need to

delve a bit more deeply than just talking about "verticals" for private

cellular, or else they risk making errors with their product portfolios

or regulatory direction.

Dean Bubley (@disruptivedean) is a

wireless technology analyst & futurist, who advises a broad range of

companies and institutions active in the 5G, Wi-Fi and cloud

marketplaces. He has covered private cellular networks for more than 20

years. He is a regular speaker and moderator at live and virtual events. Please get in touch on LinkedIn or via information AT disruptive-analysis DOT com for advisory or speaking requests.

#Private5G #Private4G #CriticalCommunications #5G #IoT #IIoT #Cloud #WiFi #verticals

We’re starting to see a trend towards multiple enterprise private 5G networks on the same site, or very close to each other. That has a lot of implications.

Various large campus-style environments such as ports, airports and maybe business parks, industrial zones and others in future, will need to deal with the coexistence of several company-specific #5G networks.

For instance, an airport might have different networks deployed at the gates for aircraft turnaround, in the baggage-handling area for machinery, across the ramp area for vehicles, in the terminals for neutral host access, and in maintenance hangars for IoT and AR/VR.

Importantly, these may be deployed, owned and run by *different* companies - the airport authority, airlines, baggage handlers and a contracted indoor service provider, perhaps. In addition there could be other nearby private networks outside the airport fence, for hotels, warehouses and car parks.

This is something I speculated about a few years ago (I dug out the slide below from early 2020), but it is now starting to become a reality.

This is likely to need some clever coordination in terms of #spectrum management, as well as other issues such as roaming/interconnect and perhaps numbering resources such as MNC codes as well. It may need new forms of #neutralhost or multi-tenant setups.

Yesterday I attended a workshop run by the UK’s UK Spectrum Policy Forum. While the main focus was on the 3.8-4.2GHz band and was under Chatham House rule (so I can't cover the specifics), one speaker has allowed me to discuss his comments directly.

Koen Mioulet from European private network association EUWENA gave an example of the Port of Rotterdam, which has 5 different terminals, 3000 businesses including large facilities run by 28 different chemical companies. It already has two #PrivateLTE networks, and 5G used on a "container exchange route" for vehickes, plus more possible networks on ships themselves. It is quite possible to imagine 10+ overlapping networks in future.

While the UK has 400MHz potentially available in 3.8-4.2GHz, some countries only have 50-100MHz for P5G. That would pose significant coordination challenges and may necessitate an "umbrella" network run by (in this case) the Port Authority or similar organisation. An added complexity is synchronisation, especially if each network is set up for different uplink/downlink splits for specific applications.

MNOs could be involved too, in roles from wholesale provision, down to just spectrum leasing. Whatever happens, regulators and others need to start thinking about this.

In the past I’ve half-jokingly suggested that a new 6G target metric should be to have “1000 networks per sq km” rather than the usual “million devices per sq km” or similar.

Maybe we should start with 10 or 100 nearby networks, but that joke is now looking like a real problem, albeit a healthy one for the private cellular industry.